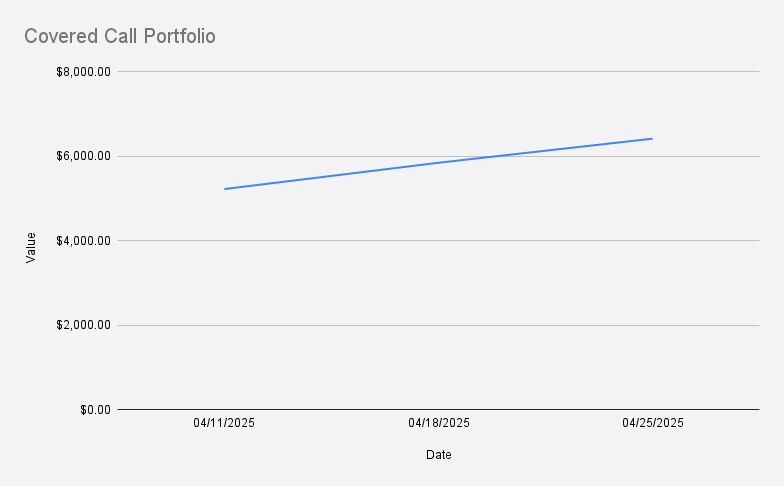

As of April 25, 2025, our covered call stock portfolio was valued at $6,411, reflecting another strong 9.76% week-over-week gain. However, it still remains down -15.87% year-to-date.

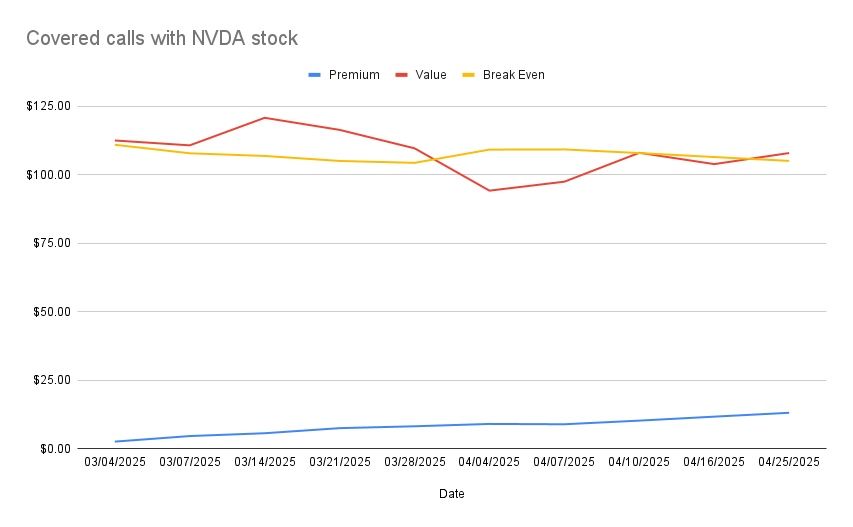

Our covered call portfolio at the moment is centered around one stock only - NVDA. I'm selling 1 covered call only, with average buy price at $118.22 (using margin), while thanks to premiums collected in previous weeks, our current break-even price is $106.53

On April 25, our covered call position was slightly in the money and, I decided to roll up and away this covered call position:

Here is the trade setup:

- Bought back the April 25 $106 call for $2.12

- Sold the May 02 $107 call for $3.54

- Premium collected: $1.41 per share

- Break-even: $105.12

Week after week we are improving our cash balance from collecting solid premium. It also incrementally moved me toward my target of owning shares outright, funded by option income.

Currently, most of these shares are financed using margin, with a total margin debit of -$6,452. While margin adds leverage and increases risk, it also allows for consistent premium capture as we gradually build the portfolio. The objective is straightforward—generate enough options income over the next 12 months to fully own the NVDA position debt-free.

Assuming an average weekly premium of $141, it would take approximately 45.75 weeks to eliminate the margin debt (excluding margin interest), We might be debt free around March 6, 2026. Encouragingly, our debt-to-cash ratio continues to improve week over week.

Subscribe to the Covered Calls newsletter to stay updated on each step of the journey!