Greetings from Latvia! This week, we skipped the last few days of school in Tbilisi and traveled to Latvia to celebrate the Midsummer Solstice. We spent time with family and friends, enjoyed the traditional festivities, had a few beers, and had an amazing time.

Back to the portfolio.

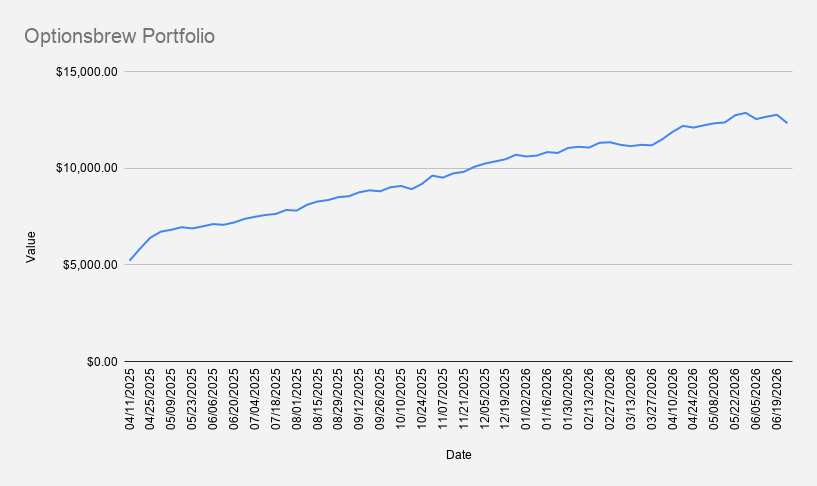

As of June 26, 2026, the portfolio value declined by 3.44% compared to the previous week, ending at $12,322. In dollar terms, that is a loss of approximately $439, making this officially the worst weekly decline since I started tracking the portfolio 64 weeks ago.

Most of the weakness can be attributed to the challenged NFLX position. Although Netflix represents only a small stock holding in the portfolio, the related options position has required several adjustments over the past few weeks. Rolling the trade has helped improve the potential purchase price, but mark-to-market losses still weighed on this week's result.

The broader market also provided little support. U.S. stocks weakened during the week, and NVDA, our main weekly options income generator, also declined sharply.

On a year-to-date basis, the portfolio is still up 20.61%, outperforming both the S&P 500 (+7.45%) and NVDA (+6.30%).

During the week, I rolled both my NFLX and NVDA positions.

As NFLX continued falling almost every day, I rolled the cash-secured put down and further out in time, lowering the strike to $66 and extending the expiration to June 2027. This has now become a very long-term position.

NVDA also lost momentum and dropped below the $200 level. I proactively rolled the 192.5/182.5 bull put credit spread one week forward. The new position is now the 187.5/160 bull put credit spread expiring on July 3, 2026.

Fortunately, Friday brought some relief, with both NFLX and NVDA recovering part of their weekly losses.

At the moment, NFLX is probably my biggest mistake in the portfolio. What started as a weekly credit spread has turned into a long-dated cash-secured put after several defensive rolls. Still, I am not looking to close the position yet.

Current Options Positions

- NVDA Jul 03, 2026 187.5/160 Bull Put Credit Spread

- LHA FRA Sep 18, 2026 7.6 Cash-Secured Put (EUR)

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NFLX Jun 17, 2027 66 Cash-Secured Put

- NVDA Jun 17, 2027 $125 Covered Call

This week's options premium came from both NVDA and NFLX, generating a total of $57.

With the current margin balance at -$2,831, it would theoretically take about 50 weeks to eliminate the debt at this pace.

Realistically, I do not expect to keep generating more than $50 per week in the coming weeks. After the recent volatility and the challenged NFLX position, I am shifting into a more defensive mode. Weekly option income may be closer to $30–40 for a while.

That is fine. The priority now is not maximizing premium, but preserving capital and managing risk.

I also continue reinvesting part of the options premium into fractional shares. This week, I added another 0.1 shares of NVDA.

Looking Ahead

Next week, the main position to watch is:

- NVDA Jul 03, 2026 187.5/160 Bull Put Credit Spread

If the position comes under pressure, the plan remains the same: roll forward when appropriate, preferably for a credit.

The NFLX position will also remain on the watchlist, although at this point it has clearly become a long-term position rather than a weekly options trade.

This was a difficult week, but the overall portfolio remains up strongly year-to-date. The focus now is simple: stay defensive, manage open trades, reduce margin debt slowly, and avoid unnecessary new risk.

Disclaimer: This article reflects personal portfolio activity and is provided for informational purposes only. It should not be considered investment advice.