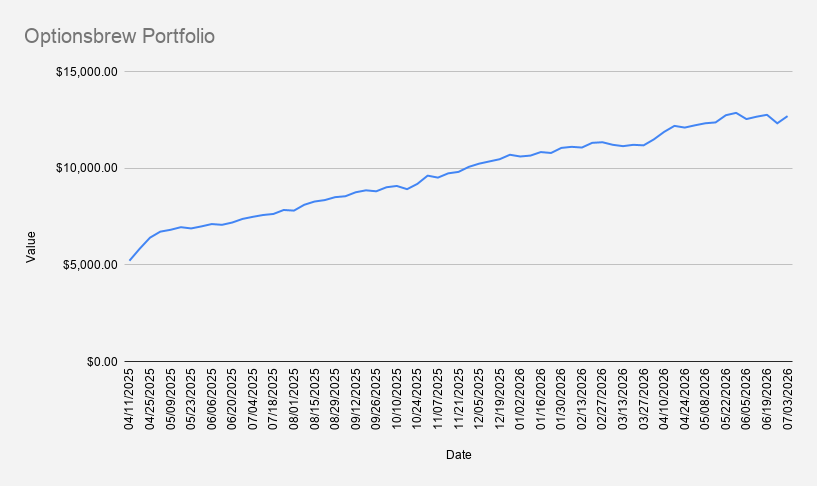

As of July 3, 2026, our stock portfolio closed at $12,693, up 3.02% week over week.

The U.S. stock market week was shortened, with markets closed on July 3 in observance of the July 4th Independence Day holiday.

But for us, the real highlight of the week was not the market. After 16 years and 3 months since I met my better half, we finally got married today in a picturesque church in Western Latvia.

It's official now!

This was a particularly good week for our stock portfolio, as both NVDA and NFLX recovered somewhat.

These are two positions I have been struggling with lately — not so much with NVDA, but definitely more with NFLX. With both tickers gaining some value during the week, the pressure on our options positions eased.

On a year-to-date basis, the portfolio is up 22.89%, outperforming both the S&P 500 (+9.11%) and NVIDIA (+3.17%).

I continue comparing the portfolio against NVDA because a significant part of the portfolio remains tied to NVIDIA exposure, both through stock ownership and options strategies.

Current Options Positions

- NVDA Jul 10, 2026 185/170 Bull Put Credit Spread

- LHA FRA Sep 18, 2026 7.6 Cash-Secured Put (EUR)

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NFLX Jun 17, 2027 66 Cash-Secured Put

- NVDA Jun 17, 2027 $125 Covered Call

During the week, I rolled the NVDA credit spread forward and down. I made the adjustment a bit earlier than usual to avoid any unpleasant surprises on the wedding day, or the day before.

Total premium collected this week was $58, part of which was used to finance the purchase of 0.1 share of NVDA stock itself.

With the current margin balance at -$2,792, it would theoretically take about 49 weeks to eliminate the debt at this pace.

Realistically, however, I do not expect to continue generating $50+ in weekly premium over the coming months.

My expectation is that weekly option income may average closer to $30–40, meaning it could take considerably longer to eliminate the remaining margin debt without selling any core stock holdings.

That is acceptable. My priority is no longer maximizing premium, but preserving capital and managing risk.

Looking ahead to next week, I will be closely monitoring the NVDA $185/170 put spread . Should any of our positions come under pressure, the plan is to roll them forward—ideally for a credit.

Never miss an update! Get weekly insights delivered to your inbox—subscribe to the Covered Calls with Reinis Fischer newsletter