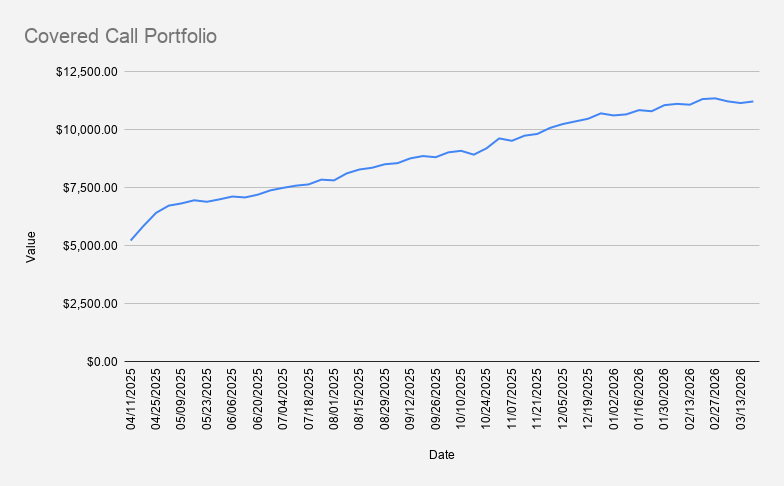

As of March 20, 2026, our covered-call stock portfolio has increased slightly by +0.62% and closed at $11,210.

For most of the week, we didn’t make any trades or adjustments. On Friday, after previous spreads expired worthless, we opened two new credit spreads on NVDA and BMY.

Additionally, we bought 0.1 shares of MCD. If you’ve been following our portfolio, you’ll know this is something we do occasionally—typically when visiting a McDonald’s.

Today was one of those days. Our 7-year-old daughter had a playdate, and we ended up at McDonald’s. I try to reinforce the idea that investing in businesses you understand and use can be sensible.

That said, the visit also highlighted an important point about tail risk. The kids were joking about suing the restaurant over improperly sized chicken nuggets—obviously not serious, but it’s a reminder. Even in companies that appear stable and well-performing, there’s always some degree of fragility and unexpected risk.

Just something to keep in mind.

Our covered call portfolio is up 7.69% YTD a healthy pullback from earlier highs while still clearly outperforming both the S&P 500 (+4.72%) and NVDA (-7.55%) over the same period.

Current options positions:

- NVDA MAR 27, 2026 165/155 Bull Put Credit Spread

- 2X BMY JUN 18, 2026 50/46 Bull Put Credit spread

- PFE MAY 15, 2026 25 Cash-Secured Put

- NVDA NOV 20, 2026 $120 Covered Call

This week was what I’d call a “booster week.” Our previous BMY credit spread expired worthless, allowing us to open a new spread with a June 18 expiry while collecting a solid premium.

Part of that premium was used to purchase 1 additional BMY share, bringing our total position to 8 shares. BMY is a dividend-paying stock, which makes it a welcome addition to the portfolio.

Similarly, from the premium collected on NVDA credit spreads, we purchased an additional 0.1 shares of NVDA—gradually increasing our core position to 101.5 shares.

This keeps the strategy consistent: use options premium not only as income, but also to gradually compound the underlying stock exposure.

One of the primary goals of our covered call stock portfolio is to gradually reduce debt while maintaining a long position of 100 shares in NVDA. Notably, we earned $171.2 in options premium this week.

This now stands as our second-best week in terms of options income. Realistically, I don’t expect to repeat anything close to this level in the coming weeks. However, if we could consistently average similar results, it would take roughly 20 weeks to fully eliminate our margin debt of -$3,557.

The goal is clear: reduce and ideally eliminate this margin debt during 2026—without having to sell any core positions. Let’s see how it plays out.

Looking ahead to next week, I will be closely monitoring the NVDA $165/155 put spread. Should any of our positions come under pressure, the plan is to roll them forward—ideally for a credit.

I’m opening up a limited number of private coaching sessions - if you want direct guidance on covered calls, cash-secured puts, or the stock market, you can book a session.

Alternatively, join my newsletter to follow along with the strategy, trades, and ongoing insights.