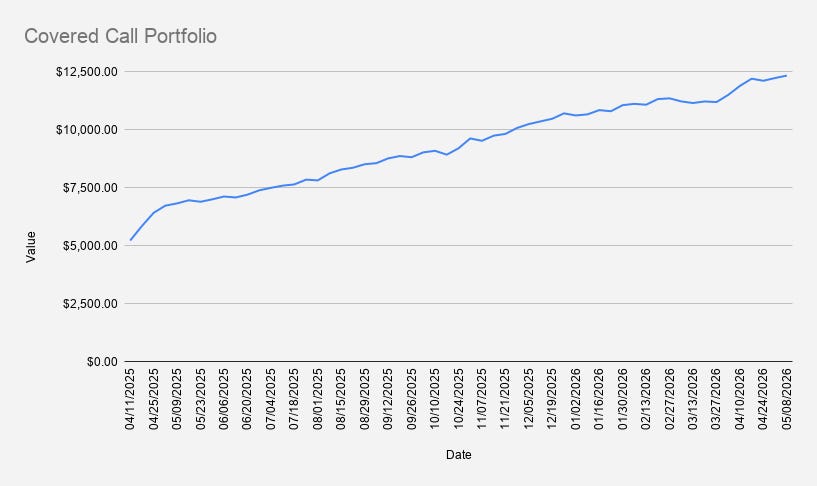

As of May 8th, 2026, our options trading driven stock portfolio increased slightly by another +0.86%, closing at $12,323.

NVDA stock surged above $215, and our previous week’s credit spreads expired worthless. I opened a new position for next week’s expiry. After such steep upward moves, I’m always cautious about placing fresh trades, since the probability of a pullback increases significantly. Nevertheless, I continued grinding our NVDA strategy to generate weekly premium income and opened another credit spread.

At the same time, I wanted to push our weekly income closer to the $100/week mark. That should become an important benchmark going forward, as the current portfolio structure can comfortably support it. The challenge, however, is finding suitable candidates that I would also be comfortable holding in the portfolio long term. That doesn’t mean there are no good stocks available — it simply means the current portfolio structure cannot tolerate just any position, so compromises are necessary.

One such compromise this week is ARCC, a stock I previously held in the dividend portfolio. ARCC is primarily a cash-flow stock with a very high dividend yield. Since options are available on it, I decided to give it a place in the portfolio and opened an additional cash-secured put with September expiry.

On a year-to-date basis, the portfolio is up 16.51%, outperforming both the S&P 500 (+7.88%) and NVDA (+13.98%).

Current options positions:

- NVDA May 15, 2026 202.5/192.5 Bull Put Credit Spread

- 2x BMY Jun 18, 2026 50/46 Bull Put Credit Spread

- PFE May 15, 2026 25 Cash-Secured Put

- DBK FRA JUN 19, 2026 24/20 Bull Put Credit Spread

- ARCC Sep 18, 2026 16 Cash-Secured Put

- NVDA Nov 20, 2026 $120 Covered Call

Using the premium collected from the NVDA credit spread and the cash-secured put on ARCC, I added another 0.1 shares of NVDA and 1 full share of ARCC. The approach remains consistent: use options income not just for short-term cash flow, but to steadily compound the underlying positions over time.

These small additions will increase our projected yearly dividend income to $63.43. Probably not the largest dividend portfolio you’ve ever seen — but the goal here is disciplined compounding, where options premium continuously finances portfolio growth without requiring additional capital injections.

A key objective of this portfolio is to gradually reduce margin debt while maintaining a core holding of 100 NVDA shares. This week, we generated $89 in options premium.

At the current pace, it would take roughly 38 weeks to eliminate the existing margin debt of -$3,324. That makes it increasingly clear that, at this rate, bringing the margin balance to zero within 2026 is unlikely. Given the current risk exposure, I’m comfortable extending that timeline into 2027, though even that isn’t guaranteed.

Another short-term goal is to increase weekly options income to at least $100 per week, while avoiding unnecessary tail risk.

Looking ahead to next week, when the PFE options expire, I’m considering adding another higher-priced but liquid stock similar to NVDA — ideally outside the tech sector. That may prove difficult, however, as most highly liquid options names tend to be concentrated in tech.

One of the candidates I’m already evaluating is NFLX for weekly credit spreads. If the PFE options expire worthless next week, I’m also considering closing the BMY credit spread and reallocating that capital into weekly NFLX credit spreads instead. That would leave the portfolio with two strong weekly premium generators — although both would be tech-related names.

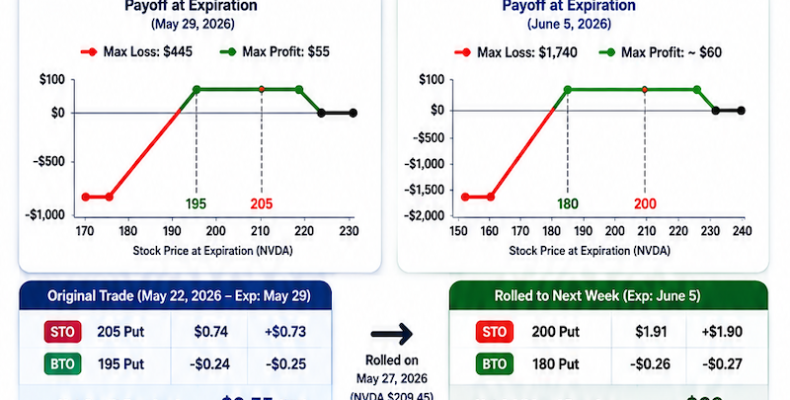

Looking ahead, I’ll be closely watching next week’s NVDA $202.5/$192.5 put spread into expiry.

If any position comes under pressure, the plan remains to roll forward, ideally for a net credit.