Blog Archive: May 2025

Week 8 / How We Collected $47 in Premiums This Week with NVDA Credit Spreads

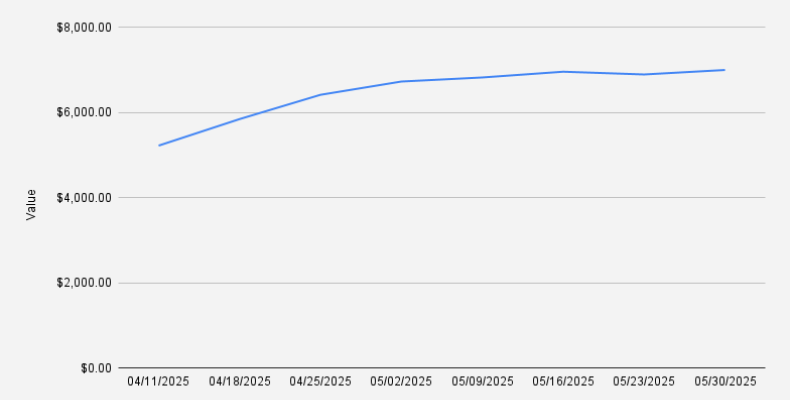

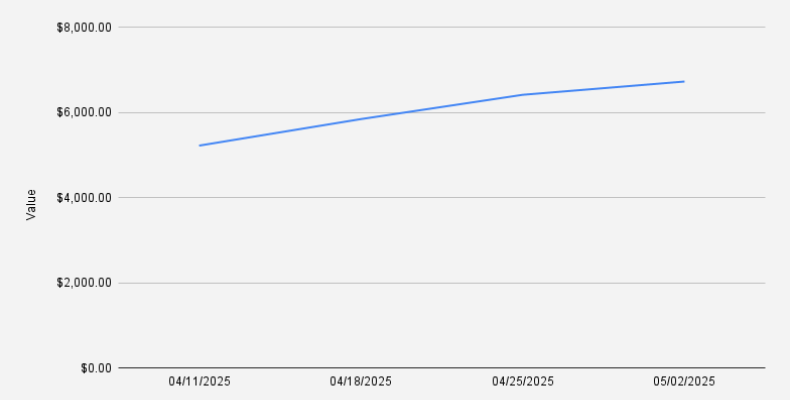

As of May 30, 2025, our covered call stock portfolio stood at $6,993, showing a +1.53% week-over-week increase (+$105). While Year-to-date, we are still down -7.26%, as we navigate volatility while optimizing our options income strategy.This week was particularly interesting—there was NVDA earning report and I discovered another options trader who is documenting his journey to $100K through weekly blog updates. I highly recommend checking it out. Since our portfolio sizes are currently similar, I find it both motivating and insightful to follow along and compare strategies as we grow together.We successfully closed a credit spread on NVDA that expired worthless, allowing us to retain the…

Larnaca International Airport

This spring, I took a memorable trip that involved connecting through three countries in less than two weeks—starting in Tbilisi, Georgia, spending a few days in Israel, and finally heading to Cyprus for a short but enriching stay. What stood out most was just how short and easy the flight was between Israel and Cyprus—a route I had never seriously considered before.Our journey began in Tbilisi, flying to Tel Aviv's Ben Gurion Airport, where we stayed for several days to visit relatives. These family moments added a personal and grounding start to what would soon shift into a more exploratory leg of the trip.After spending quality time in Israel, we boarded a short flight from Tel Aviv to…

Frame House Upgrades: Big Windows, New Porch, and Apple Trees Planted in Latvia

In mid-April, during our kiddo’s Easter school break, we traveled to Latvia for about 10 days — a trip packed with projects, energy, and transformation. A lot of pre-planning had gone into it before we even arrived: we ordered the windows, sourced the plants, and mapped out the main tasks. Once we landed, it was all about execution — and we got a lot done.One of the most transformative updates was installing our huge 3x3 meter windows. In the end I decided to split them into 1X3X3These oversized panes completely changed the feel of the house — flooding the space with natural light and giving us panoramic views of the land. Now, no matter where you stand, the outdoors feels just a step away…

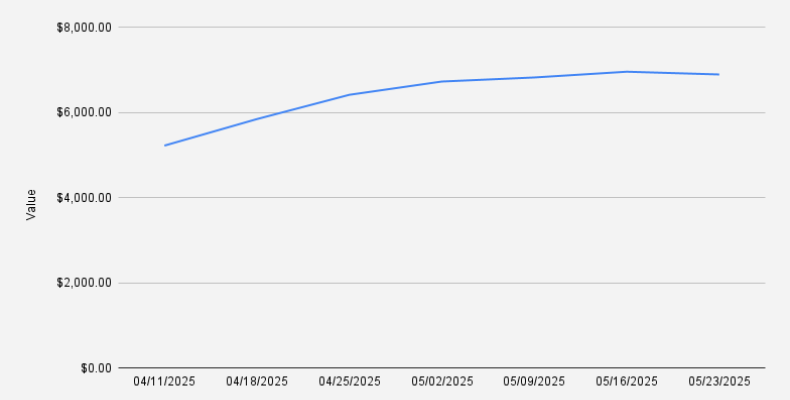

Week 7 / How I’m Using Covered Calls and Credit Spreads to Pay Off Margin on NVDA Stock

As of May 23, 2025, our covered call stock portfolio stands at $6,888, reflecting a -0.93% week-over-week decline (down $64.48). Year-to-date, we are down -9.33%, as we navigate volatility while optimizing our options income strategy.Rolling NVDA Calls for Controlled UpsideThis week, we rolled our NVDA covered call to the June 27, 2025 expiry, raising the strike to $109. Should NVDA close at or above that level at expiry, the position would yield a maximum profit of around $150. However, we remain focused on retaining the shares rather than letting them be called away. If momentum continues, we’re ready to roll the strike higher to maintain upside exposure and capture premium.Credit Spreads…

Pūre Horticultural Research Station

In mid-April 2025, we took an exciting step toward our vision of a Latvian craft cider brewery by purchasing several Antonovka apple trees and other varieties from the renowned Pūre Horticultural Experimental Station (Latvian: Pūres dārzkopības izmēģinājumu stacija).This wasn’t a random choice. Pūre is one of Latvia’s most respected institutions in plant cultivation and horticultural research. With decades of hands-on experience in the Latvian climate, they offer proven expertise in selecting trees and plants that can thrive through our seasons — cold winters, unpredictable springs, and all.Their staff provided solid recommendations not only for Antonovka, which is famous for its hardiness…

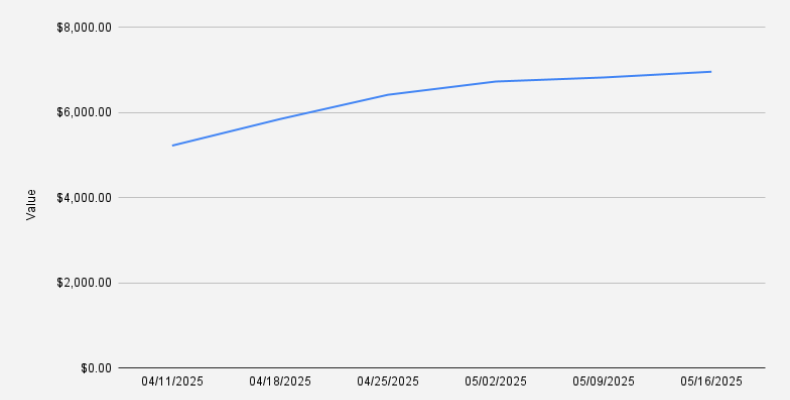

Week 6 / Doing Nothing, Gaining 1.98%: A Covered Call Strategy That Pays

In the world of trading, action often feels like progress. Placing new trades, adjusting positions, chasing setups—these behaviors can give us the illusion of control. But sometimes, the most profitable move is to simply do nothing.As of May 16, 2025, our covered call stock portfolio was valued at $6,952, reflecting a 1.98% week-over-week gain (+$134.96). That’s a modest but welcome increase, especially considering that we didn’t place a single new trade this week.Despite this recent uptick, we are still down -7.01% year-to-date, a reminder of the rocky terrain we’ve traversed in 2025. Yet even during this downturn, opportunities for calm, calculated growth remain.This week, there were no…

Samshvilde Canyon Hiking

Our go-to hiking spot in Georgia has always been Birtvisi Canyon. With its striking rock formations, narrow passages, and unbeatable views, it’s a place we return to again and again. But last Sunday, we felt like trying something new.So we picked a place we’d heard about but never explored properly: Samshvilde Canyon.In fact we almost find it few years ago, but turned our car around because the road didn't seem proper. See: Hiking at Birtvisi Canyon. This time we risked bit more. Located not far from the town of Tetritskaro, Samshvilde is known for its quiet trails and historic ruins, including the remains of the ancient Samshvilde Fortress. We packed up for a casual day hike,…

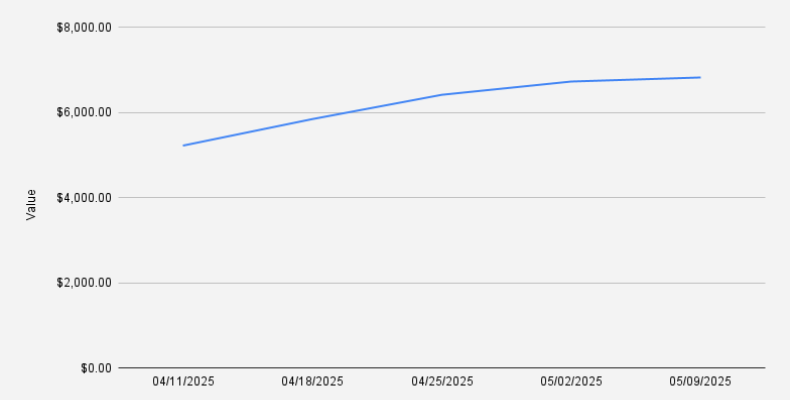

Week 5 / NVDA Rally Forces Covered Call Adjustment: Rolling Up and Out for a Credit

As of May 9, 2025, our covered call stock portfolio was valued at $6,818, reflecting another 1.42% week-over-week gain (+$95.42). Despite the recent uptick, we remain down -9.63% year-to-date.Currently, the entire covered call portfolio is allocated to NVDA stock.With NVDA rallying sharply, our May 9 $107 call moved deep in-the-money. Although my initial plan was to let the shares be called away and then re-enter via cash-secured puts, I decided to roll the position up and out for a net credit instead.Unfortunately, weekly expiries offered unattractive premiums, so I rolled into the May 23 expiration:Bought back the May 9 $107 call for $10.62Sold the May 23 $108 call for $11.03Net…

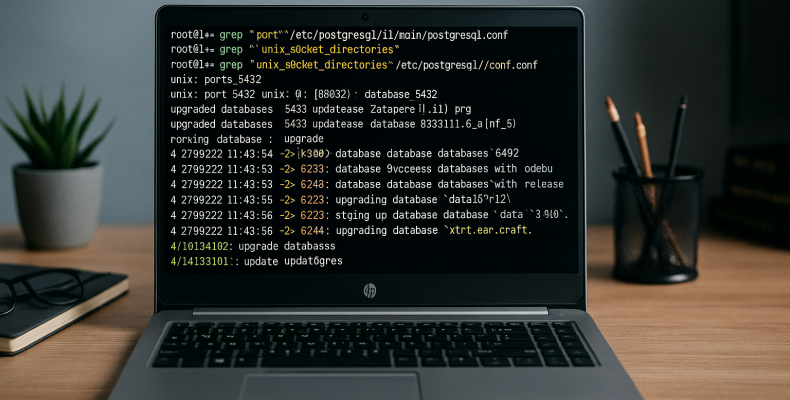

How I Upgraded XTRF on Ubuntu with PostgreSQL 14 (and Fixed Every Broken Dependency)

Upgrading an XTRF instance—especially one that has aged alongside older OS and database stacks—is never a walk in the park. In this article, I’ll walk you through the real-world path I took, upgrading from Ubuntu 18.04 all the way to 22.04, aligning PostgreSQL to a supported version, and overcoming the nuanced issues involved in deploying XTRF on Jboss. Most importantly, I’ll highlight how AI—specifically ChatGPT—helped me tackle the hard problems, including log file analysis and patching .war deployments.XTRF is a popular Translation management system we use at our Translation company in TbilisiOur system was running on Ubuntu 18.04 LTS with PostgreSQL 11, which shipped by default with…

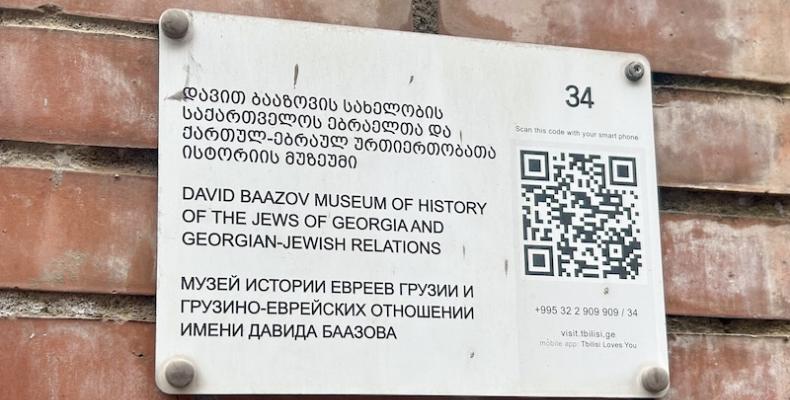

David Baazov Museum of History of the Jews of Georgia and Georgian-Jewish Relations

Tbilisi is a city full of hidden corners, rich history, and quiet treasures, one of which I recently discovered: the David Baazov Museum of History of the Jews of Georgia and Georgian-Jewish Relations.Over the years, I've gradually learned that Georgia has a deeply rooted Jewish presence. There's even a Jewish Quarter in Tbilisi, which I came across during my many walks through the city's charming old streets. Historically, Jewish communities have lived in Georgia for centuries — a fact that, at first, surprised me. My curiosity about this history grew even stronger after meeting a Georgian Jew during a visit to Israel, a moment that further highlighted the global and interconnected nature…

Week 4 / NVDA Covered Call Strategy: Earning $83 This Week To Pay of Margin Debt

As of May 2, 2025, our covered call stock portfolio was valued at $6,722, reflecting another strong 4.85% week-over-week gain. However, we still remain down -11.61% year-to-date. Our covered call portfolio at the moment is centered around NVDA stock exclusively. As of today our covered call position was in the money and, I decided to roll forward this position, Here is the trade setup:Bought back the May 2 $107 call for $7.75Sold the May 9 $107 call for $8.59Premium collected: $0.83 per shareBreak-even: $104.29I initially wanted to roll this position up and away, but since it was already deep in the money, doing so would have required either choosing a different expiry or…